Picking the cheapest premium on the screen feels like the smart move. It’s usually the fastest way to overpay.

Here’s the reality that caught millions of Americans off guard this year. To keep the exact same Marketplace plan they had in 2025, subsidized enrollees saw their net monthly payments jump an average of 114% for 2026, after the enhanced premium tax credits expired (KFF). Overnight, the “best” plan stopped being the one with the lowest sticker price. It became the one people actually understood before they clicked enroll.

Table of Contents

Choosing health insurance isn’t about finding the lowest number. It’s about matching a plan to how you and your family really use care, then checking the total cost when things go wrong, not just when they go right. Get that backwards and a “cheap” plan can cost you more than a pricier one the first time you land in the ER.

This guide walks you through the whole decision, step by step, with the current 2026 numbers our editorial team pulled from HealthCare.gov, KFF, and federal sources. By the end you’ll know exactly how to compare plans and pick the one that fits.

| Quick answer: To choose the best health insurance plan, estimate how much care you’ll actually use, then compare plans on total yearly cost (premium plus deductible plus out-of-pocket maximum), not premium alone. Confirm your doctors and prescriptions are covered, check whether you qualify for a subsidy, and pick the plan with the lowest worst-case cost for your health needs. |

| At a Glance The lowest premium often hides the highest total cost; worst-case math matters more than the monthly price.Four metal tiers (Bronze, Silver, Gold, Platinum) split premiums and out-of-pocket costs in very different ways.Plan type (HMO, PPO, EPO, POS, HDHP) decides which doctors you can see and whether you need referrals.For 2026, the maximum out-of-pocket limit climbed to $10,600 for one person and $21,200 for a family.Enhanced subsidies expired January 1, 2026, so net premiums rose sharply for most Marketplace enrollees.Cost-sharing reductions only apply if you pick a Silver plan and your income qualifies.Miss open enrollment and you usually wait a full year, unless a qualifying life event opens a window. |

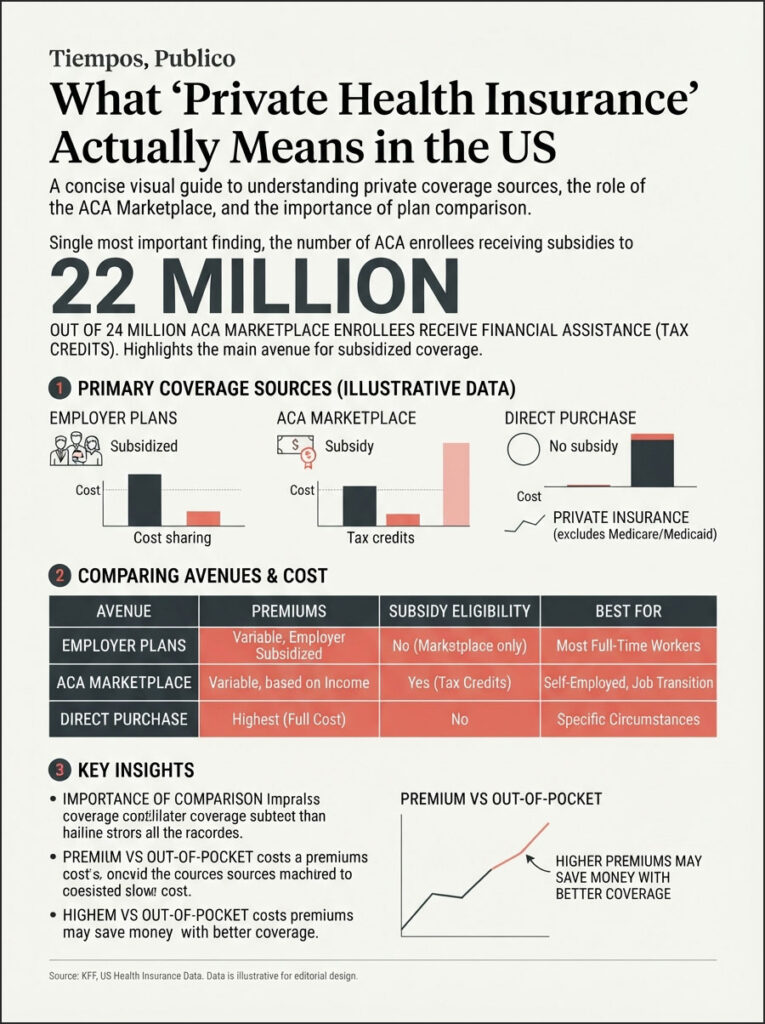

What “Private Health Insurance” Actually Means in the US

Private health insurance is any coverage that doesn’t come from a government program like Medicare or Medicaid. That covers a lot of ground, and where you buy it changes both your options and your price.

Most Americans get private coverage one of three ways. Through an employer, which usually pays a large share of the premium. Through the ACA Marketplace at HealthCare.gov or a state exchange, where you may qualify for financial help. Or directly from an insurer off the exchange, where you pay full price with no subsidy attached.

That last distinction trips people up constantly. Buy the same insurer’s plan off-exchange and you forfeit any premium tax credit you’d have earned on the Marketplace. Our review of the latest enrollment data shows why that matters so much: 22 million of the roughly 24 million Marketplace enrollees currently receive a tax credit (KFF).

Employer Plan or Buy Your Own?

If your job offers coverage, start there. Employer plans come with a built-in discount because your company pays part of the bill, and that share is money you can’t get any other way.

Still, don’t accept a workplace plan blindly. If your employer offers several options, or a spouse has coverage too, compare them the same way you’d compare Marketplace plans. Sometimes the higher-premium option at work saves money once you account for the doctors and prescriptions you actually use.

If you’re self-employed, between jobs, or your workplace offers nothing, the Marketplace is your main path to subsidized coverage. That’s where the rest of this guide focuses.

(Internal link opportunity: a full glossary of health insurance terms.)

Start With Your Real Costs, Not the Sticker Premium

The number on the plan card is the premium. It’s what you pay every month whether you see a doctor or not. It is not the cost of the plan.

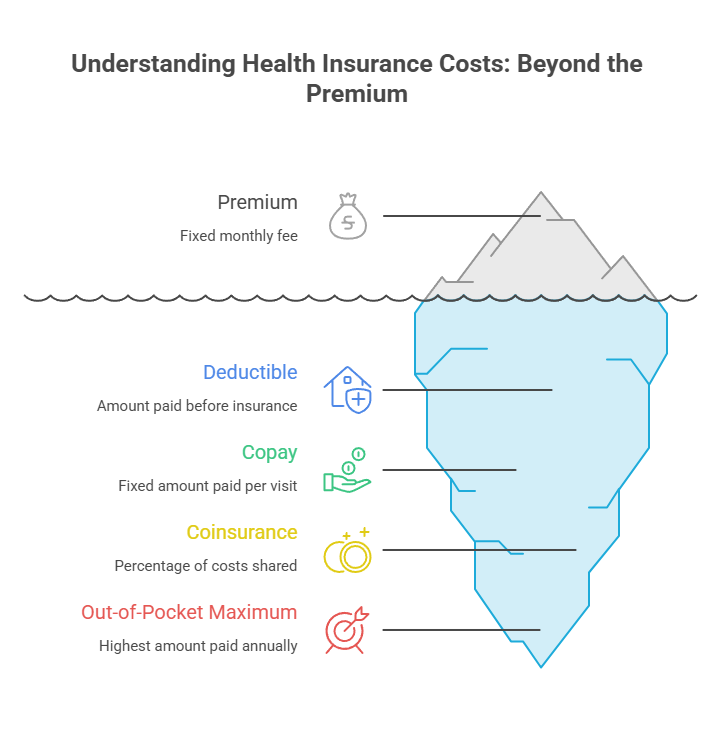

The Five Numbers That Decide Everything

Every plan lives or dies on five figures. Learn them once and comparison shopping gets simple.

Premium is your fixed monthly bill. Deductible is what you pay before the plan starts covering most care. Copay is a flat fee per visit or prescription. Coinsurance is your percentage share after the deductible. And the out-of-pocket maximum is the ceiling: once you hit it, the plan pays 100% of covered in-network care for the rest of the year.

That last number is the one shoppers ignore and later regret. For 2026, that ceiling rose to $10,600 for an individual and $21,200 for a family, up from $9,200 and $18,400 in 2025 (healthinsurance.org). Premiums don’t count toward it, and neither does out-of-network care.

The Worst-Case Math

Here’s the single most useful trick for choosing a plan. Add a plan’s total annual premiums to its out-of-pocket maximum. That sum is your worst-case cost for the year, the most you could possibly pay if your health falls apart.

Run that number for your two or three finalists. A plan with a low premium and a $9,000 deductible can lose badly to a pricier plan with a $2,000 deductible the moment you’re hospitalized. Across the plans we reviewed, the “cheap” plan and the “expensive” plan often swap places once you do this math.

The metal tiers below are built around exactly this trade-off between what you pay monthly and what you pay when you need care.

| Metal Tier | Plan Pays (roughly) | Monthly Premium | Deductible & Out-of-Pocket | Best Fit |

| Bronze | ~60% | Lowest | Highest (often $7,000+ deductible) | Healthy, low-use; now HSA-eligible in 2026 |

| Silver | ~70% | Moderate | Moderate; only tier with cost-sharing help | Subsidy-eligible or moderate care needs |

| Gold | ~80% | Higher | Low deductible, lower cost-sharing | Regular prescriptions or ongoing care |

| Platinum | ~90% | Highest | Lowest out-of-pocket when you get care | Heavy, predictable, ongoing medical needs |

| Catastrophic | Below Bronze | Very low | Deductible equals the max ($10,600 in 2026) | Under 30 or with a hardship exemption |

Note the actuarial values in that “plan pays” column: Silver plans sit at roughly 70% and Bronze around 60% of a typical enrollee’s costs (Peterson-KFF). The metal name says nothing about the quality of care, only about how you and the insurer split the bill.

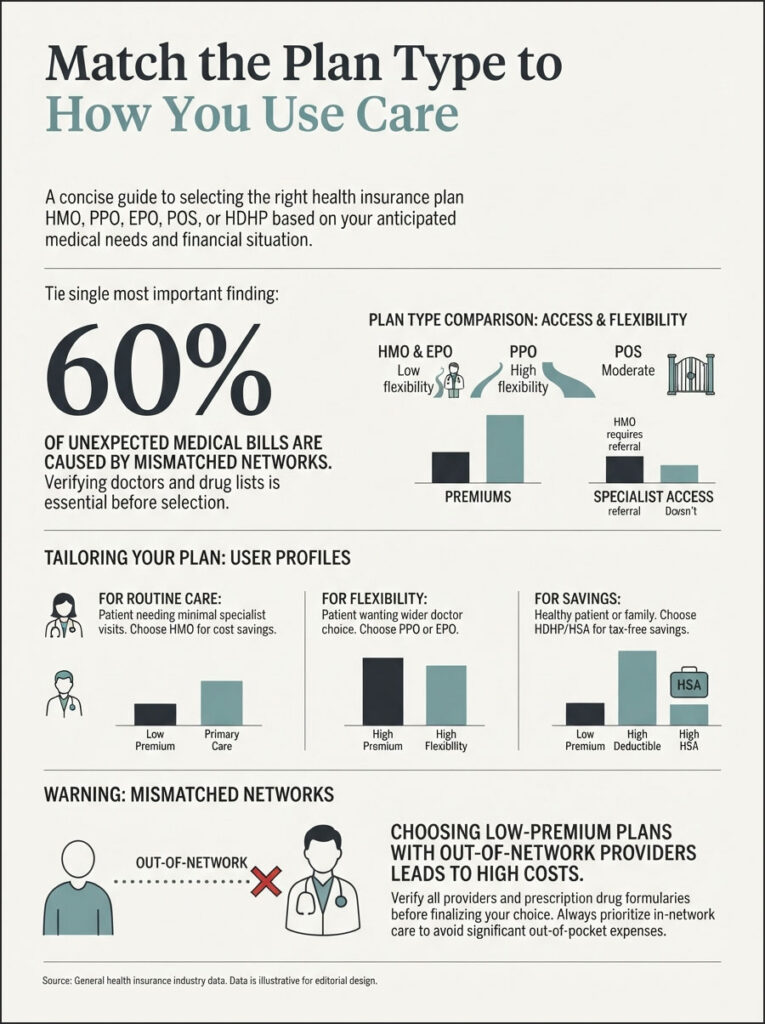

Match the Plan Type to How You Use Care

Two plans in the same metal tier can behave completely differently, because the plan type controls which doctors you can see and how you reach a specialist.

HMO, PPO, EPO, POS, and HDHP Explained

You’ll run into a small alphabet of plan types. Here’s what each one actually does.

- HMO (Health Maintenance Organization): Lowest cost, but you stick to the network and usually need a referral from your primary doctor to see a specialist. Out-of-network care isn’t covered except in emergencies.

- PPO (Preferred Provider Organization): The most flexible. See specialists without a referral, and get partial coverage out of network, in exchange for a higher premium.

- EPO (Exclusive Provider Organization): A middle ground. No referrals needed, but no out-of-network coverage either, so it often costs less than a PPO.

- POS (Point of Service): A hybrid that usually requires a referral but offers some out-of-network coverage.

- HDHP (High-Deductible Health Plan): Any of the above can be an HDHP. Lower premiums, higher deductibles, and it can pair with a Health Savings Account for triple tax savings.

When Each Type Wins

If you have doctors you refuse to give up, a PPO or EPO protects that access. If you rarely see anyone but your primary and want to save, an HMO does the job for less.

And if you’re healthy and want to bank tax-free money for future costs, an HDHP paired with an HSA is worth a hard look. HSA contributions go in pre-tax, grow tax-free, and come out tax-free for medical expenses, and the balance follows you if you change jobs.

Networks, the Mistake That Costs People the Most

A plan can look perfect and still be a trap if your doctors aren’t in it. Networks and drug lists change every year, even within the same insurer.

Before you commit, open the plan’s provider directory and confirm your doctors, hospital, and specialists are in network. Then check the drug formulary for every prescription you take, because the same medication can sit on a cheap tier in one plan and an expensive tier in another.

Picture this: you pick a low-premium plan, then learn in March that your longtime specialist is out of network. Now every visit is full price and none of it counts toward your out-of-pocket maximum. Mismatched networks are the number one cause of the surprise bills readers ask us about.

(Internal link opportunity: an in-network vs out-of-network cost explainer.)

How to Compare Your Two or Three Finalists

Once you’ve filtered down to a short list, the winner comes from a side-by-side comparison, not a gut feeling. Here’s the kind of walk-through our editorial team runs on real plan data.

Say you’re choosing between two plans. Plan A is a Bronze plan at $300 a month with a $9,000 out-of-pocket maximum. Plan B is a Silver plan at $450 a month with a $6,000 out-of-pocket maximum.

If you barely use care, Plan A wins: you’d pay about $3,600 in premiums for the year and little else. But add a surgery, and the picture flips. Plan A’s worst case is $3,600 plus $9,000, or $12,600. Plan B’s worst case is $5,400 plus $6,000, or $11,400.

So the “expensive” Silver plan is actually $1,200 cheaper in a bad year, while costing more in a healthy one. Your job is to decide which scenario is likelier for you, then pick the plan that protects that outcome. Do this for every finalist and the right choice usually becomes obvious.

Money on the Table: Subsidies, CSRs, and the 2026 Shift

For most people shopping the Marketplace, the price you see first isn’t the price you pay. Two kinds of financial help can change everything, and both shifted for 2026.

Premium Tax Credits and the 400% Cliff

Premium tax credits lower your monthly bill based on income, and most people take them in advance so the discount hits every month. The credit is tied to the second-lowest-cost Silver plan in your area, though you can apply it to any metal tier.

The catch for 2026 is the return of the so-called subsidy cliff. With the enhanced credits expired, help phases out near four times the federal poverty level, roughly $62,600 for an individual and $128,600 for a family of four (KFF). Earn a dollar over that line and you can lose the credit entirely, so estimating income carefully genuinely pays off.

Cost-Sharing Reductions, the Silver-Only Advantage

Cost-sharing reductions (CSRs) are the quietest deal in health insurance. If your income qualifies and you pick a Silver plan, CSRs shrink your deductible, copays, and out-of-pocket maximum, sometimes dramatically.

The key word is Silver. Choose Bronze or Gold and you throw the discount away. For a lower-income shopper who needs care, a CSR-boosted Silver plan can quietly outperform a Gold plan while costing less each month.

What Changed for 2026

Two shifts reshaped the math this year, and our review of the latest KFF and CMS figures shows how much they matter.

First, insurers raised benchmark Silver premiums by an average of 26%, about 30% in states using HealthCare.gov and 17% in state-run Marketplaces (KFF). Second, a rule change now treats all Marketplace Bronze and Catastrophic plans as HDHPs, which makes them eligible to pair with an HSA for the first time. If you’re leaning Bronze, that HSA door is new for 2026.

| Metric | 2026 Figure | Source |

| Max out-of-pocket (individual / family) | $10,600 / $21,200 | HHS / CMS |

| HSA-eligible HDHP out-of-pocket max | $8,500 / $17,000 | IRS |

| Marketplace enrollees getting a subsidy | ~22M of ~24M (92%) | KFF |

| Avg net premium rise to keep the same plan | +114% | KFF |

| Avg benchmark Silver premium increase | +26% (30% federal, 17% state) | KFF |

| Subsidy cliff income (individual / family of 4) | ~$62,600 / ~$128,600 | KFF |

The HDHP out-of-pocket ceiling runs lower than the general cap, at $8,500 for an individual and $17,000 for a family in 2026 (healthinsurance.org). That’s a point in favor of HSA-qualified plans if you want a firmer lid on spending.

Don’t Forget Dental, Vision, and Supplemental Coverage

Standard health plans cover a lot, but they leave real gaps. Adult dental and vision usually aren’t included, and filling those gaps is part of choosing coverage that actually fits.

You can add standalone dental and vision plans during open enrollment, either alongside your health plan or separately. If you wear glasses or expect dental work, the small monthly cost often pays for itself in one or two visits.

Some people also consider supplemental policies like accident or critical-illness coverage. These pay cash if something specific happens, and they can soften a high deductible. They’re optional extras, not a substitute for a real health plan, so treat them as add-ons only after your core coverage is set.

A 5-Step Method to Pick Your Plan

Enough theory. Here’s the repeatable process our editorial team uses when comparing real plan data, boiled down to five steps.

- Estimate your care. Look at last year. How many visits, which specialists, what prescriptions, any surgeries or conditions on the horizon? Write it down so you’re choosing on facts, not guesses.

- Set a budget with worst-case math. For each candidate, add annual premiums plus the out-of-pocket maximum. That number protects you if the year goes sideways.

- Filter by network and drugs. Drop any plan that leaves out your doctors or puts your medications on a punishing tier. This step alone eliminates most bad choices.

- Compare total cost across your finalists. Weigh premium against deductible, copays, and coinsurance for the care you actually expect, using the side-by-side method above.

- Check the quality rating and enroll. Marketplace plans carry a star rating from 1 to 5. Use it as a tiebreaker, then enroll before the deadline.

The table below turns that method into quick guidance for common situations.

| Your Situation | Plan Direction | Why |

| Healthy, rarely see a doctor | Bronze or Catastrophic with an HSA | Lowest premium plus tax-free savings for surprises |

| Regular prescriptions or specialist visits | Gold, or Silver with CSRs | Lower cost-sharing pays off when you use care often |

| Income under about 250% of poverty | Silver plan | Triggers cost-sharing reductions that cut your deductible |

| Want specific doctors, dislike referrals | PPO or EPO | Broader access and no primary-care referral required |

| Family with kids and steady checkups | Silver or Gold | Balances monthly cost against covered routine visits |

| Between jobs or recently lost coverage | Special enrollment or COBRA | A qualifying life event opens a window outside open enrollment |

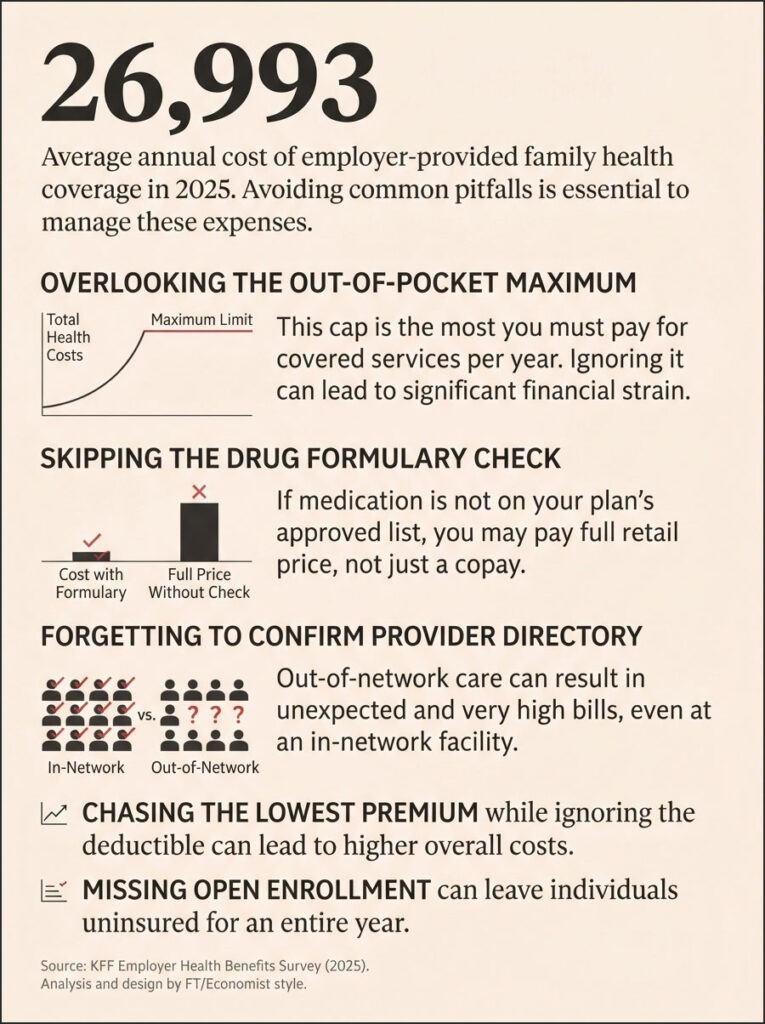

Common Mistakes That Cost People Thousands

Even careful shoppers fall into the same traps. Here are the ones readers report to us most.

Chasing the lowest premium and ignoring the deductible. Skipping the drug formulary check, then paying full price for a medication. Forgetting to confirm the provider directory, and finding out a doctor is out of network in March.

Overlooking the out-of-pocket maximum entirely. Missing open enrollment and going a year uninsured. And falling for a non-ACA “junk” plan that looks cheap until it refuses to cover something you need.

For perspective, employer coverage isn’t cheap either, even though your paycheck hides most of it. In 2025 the average total premium ran about $9,325 for single coverage and $26,993 for a family, with employers paying the larger share (KFF Employer Health Benefits Survey). If you’re buying your own plan, that context helps you judge whether a Marketplace price is fair.

When and How to Enroll

Timing is half the battle. Buy at the wrong moment and even the perfect plan is out of reach.

The Open Enrollment Window

Open enrollment for individual and family coverage generally runs from November 1 into mid-January, though exact dates vary by state. For 2026 coverage, states using the federal Marketplace closed enrollment on December 15, 2025, while several state-run exchanges ran through January 15, 2026 (Member Benefits). Enroll by the mid-December deadline in most states and your coverage starts January 1.

Special Enrollment and Life Events

Miss the window and you’re not always stuck. A qualifying life event, like losing job-based coverage, getting married, having a baby, or moving, opens a special enrollment period.

Job loss also lets you continue your old plan through COBRA, or shop the Marketplace, whichever costs less. Report the change promptly, because these windows are short and close fast.

Documents to Gather

Speed things up by having your paperwork ready. Pull recent pay stubs, last year’s tax return, and any 1099s if your income varies.

Confirm your household size and address in your Marketplace profile too, since both affect your subsidy. Self-employed and gig workers especially should estimate income carefully, because 2026 rules require repaying excess credits at tax time.

Special Situations Worth Planning For

Life changes reshape which plan makes sense, and a few moments call for extra thought. Here’s how our editorial team frames the ones readers ask about most.

Aging off a parent’s plan at 26

Turning 26 ends your spot on a parent’s plan, and that counts as a qualifying life event. You get a special enrollment window to pick your own Marketplace plan, so line one up before your birthday to avoid a coverage gap. Young and healthy shoppers often do well with a Bronze plan plus an HSA.

Self-employed or variable income

Freelancers and gig workers face a tricky task: estimating a full year’s income up front. Guess too low and you may owe credits back at tax time under the 2026 rules. Update your Marketplace profile whenever your earnings shift, so your subsidy stays accurate and your tax-season surprise stays small.

A new baby or a marriage

Both events open a special enrollment period and change your household size, which can raise your subsidy. Add the new family member quickly, and recheck whether a plan with strong maternity and pediatric coverage now fits better than last year’s pick. A growing family often shifts the math toward Silver or Gold.

Between jobs, COBRA or Marketplace?

Losing job-based coverage lets you keep it through COBRA or switch to a Marketplace plan, and the two can differ by hundreds of dollars a month. COBRA keeps your exact plan and doctors but charges the full premium your employer used to subsidize. A Marketplace plan may cost far less with a subsidy, so price both before deciding.

Nearing 65 or moving states

Approaching 65 usually means shifting to Medicare, so map your enrollment timeline early rather than defaulting into another year of Marketplace coverage. Moving to a new state changes the plans and networks available to you, and it counts as a qualifying event, so you can reselect coverage once you establish residency.

Frequently Asked Questions

Premium vs deductible, what’s the difference?

Your premium is the fixed amount you pay every month to keep coverage active, whether or not you use it. Your deductible is what you pay out of pocket for care before the plan starts covering most services. Premiums don’t count toward the deductible or the out-of-pocket maximum.

Is a higher premium or higher deductible better?

It depends on how much care you expect. If you see doctors often or take regular prescriptions, a higher premium with a lower deductible usually costs less overall. If you’re healthy and rarely need care, a lower premium with a higher deductible tends to win. Run the worst-case math to be sure.

Which metal plan is best for most people?

Silver is the most popular for good reason. It sits in the middle on premium and cost-sharing, and it’s the only tier that unlocks cost-sharing reductions if your income qualifies. In 2025, about 56% of Marketplace enrollees chose Silver and 30% chose Bronze (Peterson-KFF).

HMO vs PPO, which should I pick?

Choose an HMO to save money if you’re comfortable staying in network and getting referrals for specialists. Choose a PPO if you want to see specialists directly, keep specific doctors, or get some coverage out of network. PPOs cost more monthly but offer far more flexibility in who you can see.

How much does health insurance cost per month?

It varies widely by age, location, plan, and subsidy. Before subsidies, a benchmark Silver plan often runs several hundred dollars a month. After financial help, many enrollees pay far less; the average subsidized premium was roughly $66 a month in 2025 (KFF data). Your actual price depends on your income.

Is a high-deductible plan worth it?

For healthy people who want lower premiums and tax advantages, often yes. HDHPs pair with a Health Savings Account, where contributions, growth, and withdrawals for medical costs are all tax-advantaged. The trade-off is a large upfront deductible, so it’s a weaker fit if you need frequent or expensive care.

How do I know if my doctor is in-network?

Check the plan’s provider directory before you enroll, usually linked right from the plan details. You can also call your doctor’s office and ask directly whether they accept the specific plan you’re considering. Never assume, because networks change yearly, even among plans from the same insurer.

What income qualifies me for a subsidy?

Premium tax credits generally reach households from 100% up to 400% of the federal poverty level, though 2026 rules tightened the upper edge. For a single person that top threshold sits near $62,600, and about $128,600 for a family of four (KFF). Use the Marketplace calculator to check your exact eligibility.

What’s an out-of-pocket maximum?

It’s the most you’ll pay for covered in-network care in a plan year. Once you reach it, the plan pays 100% of covered services for the rest of the year. For 2026 the ceiling is $10,600 for one person and $21,200 for a family. Premiums and out-of-network care don’t count toward it.

Can I have two health insurance plans?

Yes, and it’s called dual coverage; for example, your own plan plus a spouse’s. One plan acts as primary and pays first, the other as secondary. It can reduce out-of-pocket costs, but you’ll pay two premiums, so weigh whether the extra coverage justifies the added expense.

What happens if I miss open enrollment?

You generally can’t buy an ACA plan until the next annual window, unless you qualify for a special enrollment period through a life event like job loss, marriage, a birth, or a move. Going uninsured leaves you exposed to full medical costs, so report any qualifying event quickly to reopen your options.

Is private insurance better than a Marketplace plan?

Marketplace plans are private insurance; the difference is where you buy. Shopping on the Marketplace keeps you eligible for subsidies and cost-sharing reductions, while buying directly off-exchange forfeits that help. For most people who qualify for financial aid, the Marketplace is the better starting point.

| Disclaimer: This guide is for general education, not personalized insurance, tax, or financial advice. Plan availability, prices, subsidies, and rules vary by state and can change. Confirm all plan details, networks, and drug coverage on HealthCare.gov, your state exchange, or with a licensed insurance agent before enrolling. |

References

- HealthCare.gov, comparing and choosing plans

- HealthCare.gov, metal categories

- KFF, 8 Things to Watch for the 2026 ACA Open Enrollment Period

- KFF, ACA insurers raising premiums by an estimated 26%

- Peterson-KFF Health System Tracker, silver vs bronze tradeoffs

- healthinsurance.org, out-of-pocket maximum

- healthinsurance.org, 2026 open enrollment preview

- KFF Employer Health Benefits data summary